The process of earning money, saving money, building wealth, and protecting assets.

Personal finance is a word that encompasses all aspects of managing your money. It could apply to something as simple as tracking your spending and saving money, or something as complex as taxes and estate preparation. (Note that this is merely one of several (types of finance.)

Money management can be stressful. In reality, 64% of Americans say they feel anxious about their finances. Nearly one-third (31%) of respondents reported greater financial anxiety in 2022 than in 2021. But consider each component separately. Master that before moving on. Personal finance is important as it comprises four crucial facets of securing your way of life:

- Generating income;

- Saving money;

- Building wealth;

- Safeguarding assets

These objectives may overlap over your lifetime. You have probably already accomplished some of the fundamentals. Knowing this can offer you confidence as you go on to another money-maximizing task.

Personal finance is not merely a textbook concept. It is the basis of your ability to live life on your own terms. For example, you should manage your cash flow such that you have extra funds. Save for the future so you can explore professional opportunities without feeling trapped in a job because you have a mountain of debt.

Understanding personal finance is liberating.

Despite the fact that two thirds of Americans report feeling anxious about their finances in 2022, there are Americans that feel good when navigating economics. Understanding how everything functions is the first step towards developing confidence.

1. Earning money

2. Managing money

3. Building a budget

4. Saving money

5. Loans and Credit Cards

6. Borrowing money

7. Your credit score

8. Taxes

9. Paying off debt

10. Insurance

11. Investing

12. Starting or managing a business

13. Travel

With a bit of preparation and a determination to make the most of what you earn, you can handle a number of financial basics on your own. Tax and estate planning, as well as investing, though often calls for professional help.

There is a high likelihood that there are millionaires in your neighborhood that you would never believe to be wealthy. They may earn significantly less than you would expect to amass such a fortune. Some folks are hardwired for frugality. Most of us must exert considerable effort to save a few dollars. This is where the adage "it's not what you make, it's what you keep" applies.

Here are some key personal finance concepts related to that:

What you can spend is your take-home pay, or net income after all deductions. It is the foundation of your budgeting strategy. It is important to know how much money you will receive after insurance, taxes, and benefits are deducted because you only spend what you have in the bank.

Money. Who doesn't need more? A little extra money can go a long way. At the end of the day, there’s only so much that you can cut out of your budget, but the amount you can earn is almost limitless. Increasing your income can help whether you're saving for a down payment, planning a wedding, paying off debt (oh, student loans! ), or putting money away for a rainy day. Your side hustle can help pay for expenses. A side gig from home will make a difference in your wallet and provide you independence.

Here are some great ways to earn money online!

Over 6% of U.S. households don't have a checking or savings account at a bank or credit union. But if you know how to choose the best bank accounts, you can save more money and spend less.

This is a type of deposit account that you can open at a brick-and-mortar bank, an online bank, or a credit union. Checking accounts let you put money into them, which you can then use to pay bills or buy things. You might also call them transactional accounts. They are different from savings accounts because they are not meant to hold money for a long time. Instead, they are meant to be used every day. The money you keep in your checking account is money you plan to use in the short term to pay your bills.

A savings account is a deposit account designed to hold money you don't want to spend immediately. This is different from a checking account, which allows you to write checks and make purchases and ATM withdrawals with a debit card. Savings accounts help you save towards goals. You can open a savings account for an emergency fund or a down payment.

Opening a certificate of deposit is a good way to get a guaranteed return on your money with little risk. CDs tend to have the highest interest rates of all bank accounts, and unlike stocks and bonds, they are insured by the government.

The American Dream includes buying a home. Buying or renting affects your finances, lifestyle, and personal aspirations. Your choice relies on your lifestyle and budget. Both require a regular income (to fund payments and fees) and some effort to maintain. Click here to connect with an advisor.

Budgeting systems are made to help you understand your relationship with money and figure out how to improve it. Even though they all have the same goal, they often use different ways to get there.

How to choose the best way to make a budget? Click here.

When you lend out money, you get paid interest, and when you borrow money, you pay interest. In a nutshell, it's the fee charged for the right to use someone else's money.

An ‘emergency fund’ is money that is set aside to pay for big, unexpected costs like:

- Unexpected bills for health care

- Repair or replacement of home appliances

- Major car fixes

- Unemployment

A health savings account, or HSA, is a good way to save money for medical costs and lower your taxable income at the same time. But not everyone can or should sign up for the kind of health insurance plan that is needed to open an HSA.

A 529 plan can be a great way to save for college if you know the rules and how to make the most of your investment. A 529 plan is a type of savings and investment account where money grows tax-free as long as it is used for qualified education costs. It was named after a section of the IRS code. 529 plans come in two different kinds. Find out more about 529 plans and see a list of them by state. However, there are several ways to save for college. A 529 may not be the best option in your particular situation.

Find out how much you'll need for a down payment, find ways to save money, and put your savings in the right type of account. Check out our first time home buyer’s tips blog here.

Credit card selection is part art, part science. No credit card is best in all categories or for everyone. By knowing your options and asking the proper questions, you can choose the best card for your spending and credit.

Here are some credit card tips from resident financial planner, Renee Marinez.

Get help finding the right vehicle loan — and make sure to utilize all your options if you're having trouble. Connect with us here for guidance on affordability, down payments and fees.

Should you refinance your student loans? If so, how can you find the right lender or the right payment plan? Resident experts, Josh and Jen have put together all the resources you need to answer these questions and more.

Check out these videos for the latest updates:

Who Qualifies For Student Loan Forgiveness under Biden's Expansion?

PSLF Limited Waiver Changes: What You Need To Know

Personal loans often carry fixed annual percentage rates between 6% and 36%. The loan with the lowest interest rate is typically the most cost-effective option. Other factors, such as no fees, mild credit checks, and whether lenders pay your creditors directly if you're consolidating debt, set some loans apart. We spend countless hours analyzing loans from over 30 personal loan providers to discover the best interest rates and loan features. Connect with us here if you need guidance.

Finding the best mortgage for you is simple when you compare them. Whatever your home buying goals are, we’ve got the tools, calculators, and nerdy know-how to help you tackle them.

- Compare mortgage rates.

- Get pre-approved.

- Calculate your mortgage payment.

- Explore refinance options.

- Estimate your home's value.

- Find the best lenders for mortgages.

It is commonly believed that homeownership increases wealth. What is home equity, and how does it increase your net worth? Your home's equity is its current market value minus your mortgage balance. You need a positive number.

Any profit results from: 1) Paying down the loan's principal balance. 2) A sustained increase in market worth.

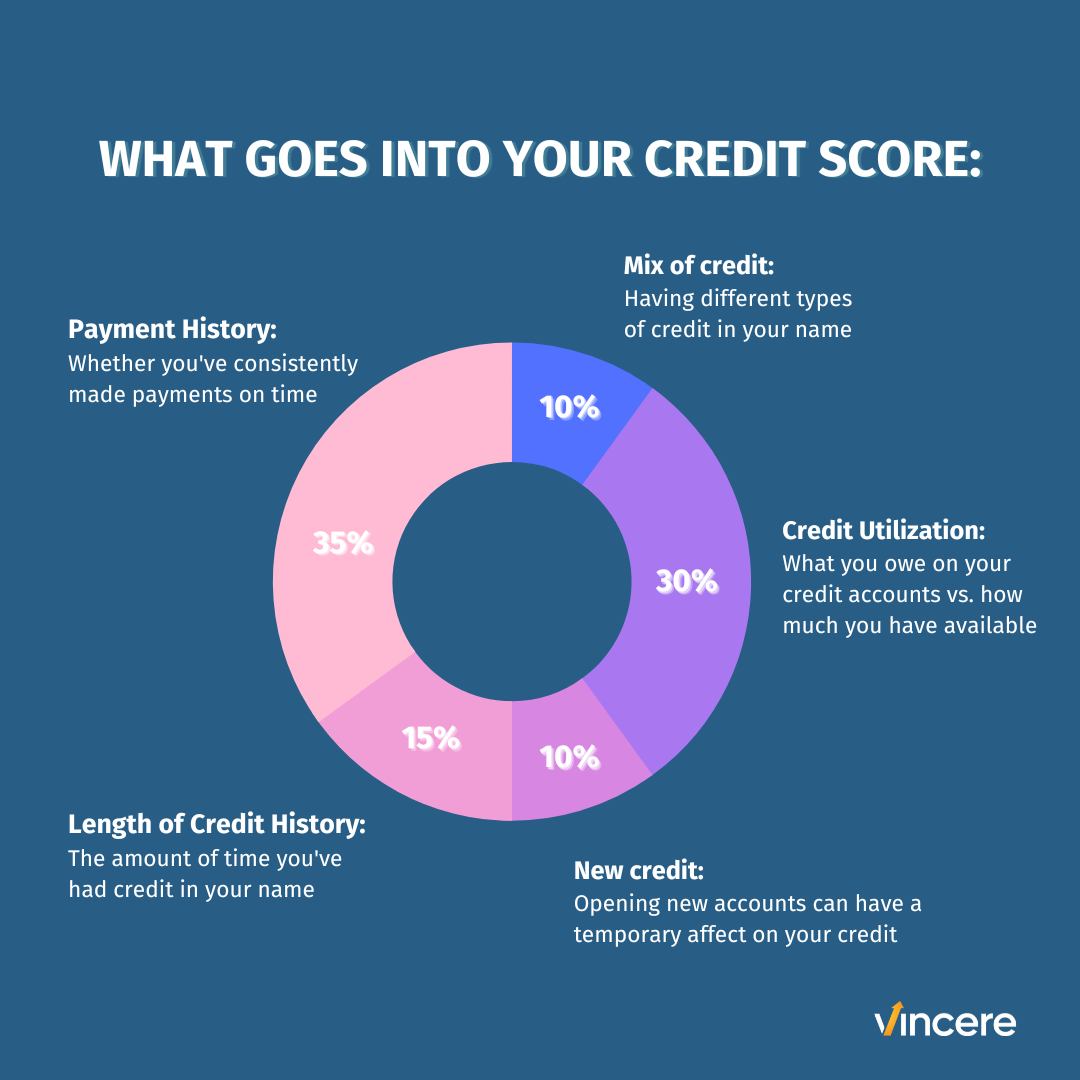

A credit score is a number that lenders use to assess the risk associated with lending you money or issuing you a credit card. Creditors use your credit score and other factors, such as your debt and income, to determine whether to approve your credit application and to determine the interest rate.

The two factors that have the most impact on your credit score are whether you pay your bills on time and how much of your available credit you use (less is better).

Without a credit history, it might be difficult to obtain a loan, credit card, or even an apartment. But how are you to show a history of responsible repayment if no one will extend credit to you?

It is important to monitor your credit history since it can influence how much you pay for vehicle or home insurance, your ability to rent a house or apartment, and even your chances of getting some jobs.

Monitoring your credit is similar to checking your blood pressure to see how your new fitness routine and diet are affecting it. It's doubtful that you'll witness continuous, uninterrupted improvement, but it can tell you if you're on the correct course. If your credit score or reports change a lot and you don't know why, you should pay attention. It could be a sign of identity theft or a mistake on your credit reports.

Credit repair can be more difficult than starting from scratch. You're trying to demonstrate to lenders and credit card issuers that, despite past mistakes or unavoidable circumstances, you're highly likely to make future payments on time.

Tax planning is the art of setting up your finances so that you can avoid or put off paying taxes. If you plan your taxes well, you can save and invest more money or just have more money to spend. Or both. Your choice. In other words, tax planning means delaying or completely avoiding taxes by taking advantage of helpful tax law provisions, increasing and speeding up tax deductions and tax credits, and generally making the most of all applicable breaks in our beloved Internal Revenue Code.

Seeking professional tax advice before pulling the trigger on significant transactions is usually money well spent. Connect with our affiliate, tax firm, Vincere Tax here.

Most put off making a plan to pay off their debt. But if you have the right tools and motivation, you can probably get out of debt sooner than you think! Our debt pay-off strategy can help you get control of your liabilities. This strategy shows you when you will be debt-free with your current payments and how much faster you will get there if you pay more each month. We also look at the differences between the debt snowball and debt avalanche strategies.

Check out Isaiah’s video: 6 Debt Myths Debunked

You're in a great position if you're thinking about paying off your mortgage. That's assuming you've saved as much as you can for retirement, set aside money in case of an emergency, and have a big chunk of cash to put toward your home loan. Or maybe you're thinking about a faster payment plan to get rid of your mortgage faster. You might want to pay off your mortgage for many reasons, but should you?

Not sure if you owe too much money? To figure out your debt-to-income ratio, add up all of your monthly debt payments, like car loans, credit card payments, and child support, and divide by your monthly income. Higher DTIs can be hard to pay off and can make it hard to get new lines of credit.

For example, a DTI of more than 43% may be too high and mean you need help with your debt.

No matter how hard you try, you can't seem to get ahead of your debt? If so, you might have too much debt to pay off. Look into your options for getting out of debt if you want to get rid of this financial burden. These tools can change the terms of your debt or the amount you owe so you can get back on your feet faster. But debt relief programs aren't the best option for everyone.

Learn about your options and the effects of getting out of debt.

Risk can be transferred through insurance, but at a cost. In the event of death, injury, disability, or property damage, you pay a company to accept a limited risk. It is a cornerstone of personal finance. Depending on your family's needs and your level of wealth, your insurance needs will change throughout the course of your life.

Life insurance protects anyone financially dependent on you. If you die unexpectedly, life insurance can replace your salary, pay off your mortgage, cover your children's college tuition, or any other expense you want to cover.

Your house is more than just a place to sleep. It could be your most valuable possession — and one you won't be able to replace out of pocket if disaster strikes. That is why it is critical to secure your investment with the proper homeowners insurance coverage.

Car insurance costs $1,630 a year, on average. Your auto insurance rates can go down, among other things, if you shop around for quotes more often.

Annuities are financial products that can help make sure you have a steady income after you retire. But an annuity can be a complex creature.

Even though it's hard to think about now, it's likely that you'll need help taking care of yourself in the future. How will you pay for it? That's the big question.

One way to get ready is to buy insurance for long-term care. Long-term care is a broad term for a number of services that regular health insurance doesn't cover. Long-term care insurance helps pay for the costs of care when you have a long-term illness, a disability, or a disease like Alzheimer's.

To buy stocks, you first need a brokerage account, which we can set up for you. Then, once money is added to the account, we can guide you through the process of finding, selecting and investing in individual companies.

An IRA, or individual retirement account, is a tax-advantaged investment account that people use to save for retirement. Some IRAs may let you pay less tax on your contributions or on the money you take out.

IRAs come in different forms, such as traditional, Roth, SEP, and SIMPLE.

When you invest through a standard brokerage account, also called a "taxable account," there are no tax benefits. Most of the time, your investment earnings will be taxed. On the plus side, this means that these accounts have very few rules: You can take out your money whenever you want and invest as much as you want.

- Mutual fund investors own shares in a company that buys shares in other companies as its main business (or in bonds, or other securities). Investors in mutual funds don't own the stocks of the companies the fund buys, but they do share equally in the profits or losses of the fund's total holdings. This is why mutual funds are called "mutual."

- Exchange-traded funds can be bought and sold like individual stocks, but they have the benefits of diversification that come with mutual funds. Most of the time, the minimum investment for ETFs is lower than it is for index funds.

Fixed-income investments, like government and corporate bonds, can provide a steady, predictable source of income, and they often have less risk than other investments. Along with stocks and stock mutual funds, fixed-income investments are the backbone of a well-diversified investment portfolio.

From planning to loan selection, we'll help you connect with the right advisor so you can take care of your business.

Dreaming of a vacation? We have the tools and tips to help you compare and find the best travel credit cards and loyalty programs to make your next trip as budget-friendly as possible.

Creating wealth should not be difficult, ineffective, or expensive. We move mountains in order to facilitate your growth with clarity and simplicity. Defending your aims. Protecting your time. Defending your aspirations.

We are devoted to fighting for you as your stewards.

Personal finance can be extremely overwhelming, given that it encompasses all financial decisions made throughout one's lifetime. But rest assured—it doesn't have to be difficult! When you break personal finance down, you'll find that it can be done in very simple steps that you can and will master. To find out more about the fundamentals of personal finance, keep reading.

Personal finance can be extremely overwhelming, given that it encompasses all financial decisions made throughout one's lifetime. But rest assured—it doesn't have to be difficult! When you break personal finance down, you'll find that it can be done in very simple steps that you can and will master. To find out more about the fundamentals of personal finance, keep reading.

Personal finance can be extremely overwhelming, given that it encompasses all financial decisions made throughout one's lifetime. But rest assured—it doesn't have to be difficult! When you break personal finance down, you'll find that it can be done in very simple steps that you can and will master. To find out more about the fundamentals of personal finance, keep reading.

.svg)